The massive money creation in the 2000s has led to a debt and asset bubble, which is about to burst. Investors will be shocked by the speed of the decline and won’t react before it is too late.

The massive money creation by central and commercial banks in this century has resulted in a growth of global assets from $450 trillion in 2000 to $1,540 trillion in 2020.

DEBT TO GDP GROWTH

As the chart below shows US debt to GDP held well below 25% from 1790 to the 1930s, a period of almost 150 years. The depression with the New Deal followed by WWII pushed debt to GDP up to 125%. Then after the war, the debt came down to around 30% in the early 1970s.

The closing of the gold window in 1971 ended all fiscal and monetary discipline. Since then, the US and much of the Western world has seen debt to GDP surge to well over 100%. In the US, Public Debt to GDP is now 125%. Back in 2000 it was only 54% but since then we have seen a vote buying system with a money printing bonanza and an exponential increase in debt to 125%.

A major part of the debt increase has gone to finance the rapid growth in property values.

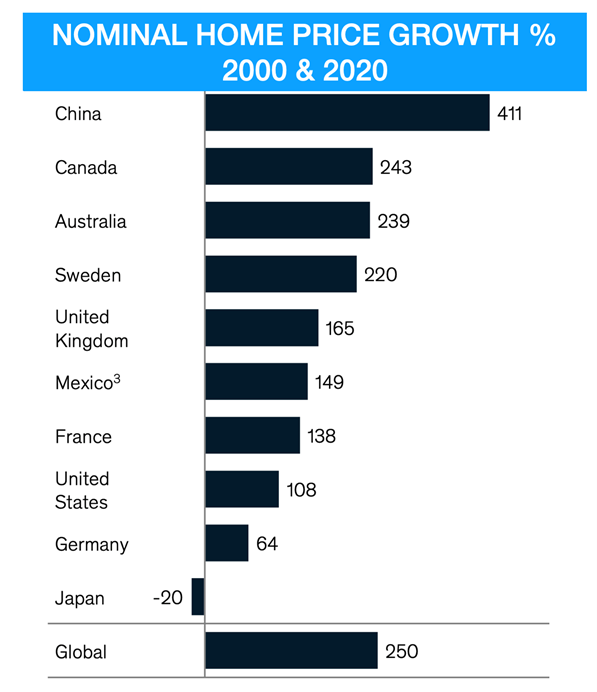

The table below shows that property has grown on average by 250% between 2000 and 2020. So individuals are creating wealth by swapping properties with each other. Hardly a sustainable form of wealth creation.

The exponential growth in property prices has been global although countries like China, Canada, Australia and Sweden stand out with over 200% gains since 2000. Most of the properties bought in the last 20+ years involve massive leverage. When the property bubble soon bursts, many property owners will have negative equity and could easily lose their homes.

…click on the above link to read the rest of the article…