Home » Posts tagged 'david haggith'

Tag Archives: david haggith

Markets Are Biting Their Lips over Global Chaos

Markets Are Biting Their Lips over Global Chaos

And Fed Chair Powell is joining them because suddenly nothing is going right for his soft-landing plans!

Rising Middle-East tensions are driving up the price of crude oil and driving down the price of stocks and value of bonds. Analysts are saying oil could go to $100/bbl if the conflict between Israel and Iran goes any further. If Israel responds to the recent attack by Iran, some think Iran is likely to fight back with the West in a variation of what it has already done via its proxies. In the worst-case scenario for oil, Iran will block the Strait of Hormuz to tanker traffic, using its proxies to do there as they have already done on the other side of the Arabian Peninsula (or doing that directly, themselves, from Iran). That could raise oil to $130/bbl, which would blow the doors off inflation. Societe Generale puts the risk at $140/bbl if the US gets involved. For now, however, the oil market is just biting its lips … like this:

Well, that’s Fed Chair Jerome Powell, but he is biting his, too, as everything turns against his flight plans for a soft landing at the end of his own war … with inflation.

That’s because the Fed pumped so much money into the economy during the Covid lockdown fiasco that he can’t get the surplus money out quickly enough. As noted yesterday, and caught in the news again today, Powell has clearly pushed rate cuts back once again. In fact, Bank of America is now resetting its calendar for the first cut to March of next year (going for a different March than the one most analysts originally thought they would get…

…click on the above link to read the rest of the article…

Forget the Black Swans; the Vultures already Circling us Are Bad Enough to Kill us

Forget the Black Swans; the Vultures already Circling us Are Bad Enough to Kill us

There is certainly more coming to eat away at your finances as infamous bankster Jamie Dimon laid out quite broadly and plainly this week.

Jamie Dimon never saw a dying bank he didn’t want to eat. Yet, while I think that Dimon’s name should be pronounced less like the clear, crown jewel of choice and more like the horned fiends of Hades, he does often speak of things likely to bring down the banking world or the economy with more candor than any other bankers, including particularly his partners in crime at the Fed. And you can be sure he has his scavenger eye on those things.

Perhaps it is just because he has unparalleled confidence that he is untouchable like a serial killer who talks to police on the street about how sorry he feels that they have had no luck at all finding the serial killer. He’s just that confident his next big take from hauling in a failing bank at fire-sale prices is so certain, he needn’t worry that warning everyone of the coming failures will get in the way of his business. Thus, he can play the saint for warning us all, knowing the greedy will ignore his warnings anyway, and still wait in the wings for that Friday evening call from Fed Chair Jerome Powell that says, “We have another bank for you. Can we meet tomorrow morning to discuss terms and complete a weekend sale?”

Fitting right in with my theme for this weekend’s Deeper Dive for paying subscribers to be titled “The Apoceclypse,” The CEO of JPMorgan Chase warned the world this week that it faces “Risks that eclipse anything since World War II.” I, of course, couldn’t agree more, so I want to spend this article distilling the Dimon’s annual report down to the most essential risks:

…click on the above link to read the rest of the article…

Inflation is Causing Tectonic Shifts

Inflation is Causing Tectonic Shifts

Even if stock investors are acting as if nothing happened along the road they are walking, they will soon wish they had not missed the obvious.

Yesterday when stocks crashed hard, I wrote the following caveat to their epitaph:

Whoa! Delusions broken. At least, for today, but give investors a wisp of faint hope tomorrow, and greed may go from free fall to free floating again.

Indeed, the faintest wisp was all they got in today’s PCE inflation report, but that was all it took to send them deliriously positive in a state of euphoria and denial again. That won’t likely last long, foolish as it is, because the road is likely to be more than bumpy from here on out on the inflation front—more like jagged—and because bond investors today refused to give up the tougher edge they took yesterday with the bond vigilantes holding out for better returns. Never underestimate the foolishness and denial that undergirds this stock market, causing investors to miss the obvious signs on each side of them.

… Because, as I also wrote yesterday …

The 2YR yield is now getting very close to 5%. At those levels Treasuries will be seriously sucking money out of stocks for the practically free ride of doing nothing but sitting home with zero risk and clipping interest coupons. Those days won’t be long in coming.

That is what we saw today in bond action as yields continued to rise. A few articles in the news today highlighted how bond traders are now demanding higher yields from US Treasuries and not letting go of the reins…

…click on the above link to read the rest of the article…

No Bubble Here, Folks!

No Bubble Here, Folks!

Anyone see a bubble anywhere? This is short and sweet because the picture says it all: We’ve just seen the fastest, highest rocket ride in stocks in the history of the world! Because that makes sense during a time of global plague and global economic lockdowns, creating extreme labor shortages, resulting in extreme product and materials shortages because 10% of the labor force has quit for good or been fired under the Biden Mandates. The present stock-market bubble makes the 1987 crash look like a pimple on the flank of the Himalayas! Anyone see where Mount Everest is in that picture? What could possibly go wrong??? But, hey, this is NOT a bubble created from Fed money laundering — uh, I mean printing, uh, I mean keystroking! If you believe that, you fully deserve everything that happens to you when the bubble bursts!

Anyone see a bubble anywhere? This is short and sweet because the picture says it all: We’ve just seen the fastest, highest rocket ride in stocks in the history of the world! Because that makes sense during a time of global plague and global economic lockdowns, creating extreme labor shortages, resulting in extreme product and materials shortages because 10% of the labor force has quit for good or been fired under the Biden Mandates. The present stock-market bubble makes the 1987 crash look like a pimple on the flank of the Himalayas! Anyone see where Mount Everest is in that picture? What could possibly go wrong??? But, hey, this is NOT a bubble created from Fed money laundering — uh, I mean printing, uh, I mean keystroking! If you believe that, you fully deserve everything that happens to you when the bubble bursts!

Why M1 Money Supply (Cash) is Skyrocketing Like No Time in History

Why M1 Money Supply (Cash) is Skyrocketing Like No Time in History

In my last Patron Post, which I eventually made available to everyone, I revealed a little-known (at the time) fact that M1 money supply (the most liquid forms of cash — bills, checks and basic savings accounts) had grown faster than any time in history. I showed that using a graph like the following, which is now brought up to the most current data:

In my last Patron Post, which I eventually made available to everyone, I revealed a little-known (at the time) fact that M1 money supply (the most liquid forms of cash — bills, checks and basic savings accounts) had grown faster than any time in history. I showed that using a graph like the following, which is now brought up to the most current data:

With part of December now in the picture, you can see the faintest hint at the top of the steep late-November climb that shows the climb may be rounding off.

I noted,

That is a massive amount of new cash money — historically massive — done almost covertly in the quickest burst ever — and yet it did not even cause the stock market to blink!… The graphs … make it clear why inflation under the new regime could become a much more serious problem than the limp moves seen over all the years of the Great Recovery, the difference being how fast the Fed’s QE is now converting into cash

… and I asked,

Why did such an enormous surge in money supply happen in the last two weeks of November with no financial articles being written about it and no statements from the Fed about it? What is going on behind the scenes at the Fed and/or US treasury right now?

…and I promised I would look into and get back to you on it.

I think that I may have found a couple of answers, so I am getting back to you on that as promised.

This could be due to Biden’s promised termination of tax welfare to the rich

…click on the above link to read the rest of the article…

Pandemic Pandemania Causes Global Economic Crisis

Pandemic Pandemania Causes Global Economic Crisis

Back in the oil-embargo recession of the early 70s when Boeing was Seattle’s economy and was laying off thousands of Seattleites, a billboard on the edge of town by Sea-Tac Airport read, “Will the last person leaving Seattle turn the lights out?” (Boeing had gone from 100,800 employees in 1967 to 38,690 in 1971.)

Since Seattle is the first area where the coronavirus made landfall in the US, I’ll present Seattle’s viral transformation in the last forty-eight hours (about two weeks since the first cases were reported) as an anecdote for the extremely rapid changes already sweeping many cities in the US as outbreaks begin to show elsewhere.

You may recall I recently wrote that the COVID-19 virus, whether it grew to become one of the world’s great killers or just the cause of one of the world’s great panics, would certainly bring rapid economic damage. It would also help take down the stock market by accelerating us into recession, which is how I’ve been predicting this bull run will finally die. (See “COVID-19 (Coronavirus) Economic Impact Sweeps Down on Global Economy Like a Fat Black Swan.”)

The crisis has now become economic suicide because it is not the death of millions of people that is tearing the economy apart; it is the fear that there may be deaths of millions of people that is causing humanity to tear the already fragile fabric of the global economy apart with actions taken on the political level, the corporate level and the individual consumer level. It is a fabric already worn thin by two years of trade wars, moth-eaten by corruption and greed, and badly woven in the first place from materially flawed economic ideas, patched with bailouts.

…click on the above link to read the rest of the article…

Dr. Fed Frankenstein Kept Alive by Zombies

Dr. Fed Frankenstein Kept Alive by Zombies

Did you know Dr. Frankenstein created a monster that stays alive to this day by eating zombies? Neither did the zombies. Neither, apparently, did Dr. Frankenstein. In fact, the zombies, being braindead as zombies are, do not realize that they are also keeping alive the diabolical doctor who made the monster that is eating them.

This little article, however, is going to tell you how all of that has become the strange case of the world as we all know it today. And, at the end of the article, I’m going to give everyone access to the first “Patron Post” I wrote as my thank-you to supporters who chose to keep this blog alive at the close of last year. That post was titled “2019 Economic Headwinds Look Like Storm of the Century.”

Before I do, I want to recap 2019 by shining a light on the occulted diabolical nature of the single most important economic event this past year … so that you can read the article in an appropriate frame of mind. You would not, after all, watch a horror movie without first turning out the lights to set the mood. In this case, however, I must also turn on a single small lamp to shine a light on the face of the monster hidden the dark corner of the banking world. Then we will be ready to review the article in context of all that transpired.

One purpose I had for laying out what I thought would be the prevailing headwinds in 2019 was, of course, to help people realize what they should keep their eyes on for their own sakes. That may or may not give them information they factor into investment decisions, but investments decisions are not at all what this blog is about.

…click on the above link to read the rest of the article…

Repocalypse: The Second Coming

Repocalypse: The Second Coming

This little monster that feeds beneath the surface of global banking at its core briefly raised one ugly eye out of the water as 2018 turned into 2019. I wrote back then that the interest spike we saw in the kind of overnight interbank lending known as repurchase agreements (repos) was just the foreshock of a financial crisis being created by the Fed’s monetary tightening. I said the Fed’s continued tightening would eventually result in a full-blown recession that would emerge, likely out of the repo market, sometime in the summer. In the very last week of summer, the Repo Crisis raised its head fully out of the water and roared.

When I first wrote of these things at the start of 2019, the Fed had only been up to full-speed tightening for three months, and already it was blowing out the financial system at its core. The stock market had just crashed with the onset of full-speed tightening just as I had said it would. It fell hard enough to where the only index holding just one nostril above the icy water was the S&P 500 at a 19.8% plunge. Even that holdout briefly dipped its last air-hole under water in the middle of the day (i.e., below 20%), but didn’t stay below for the count. All other major indices and most minor ones took the full polar-bear plunge into the deep, dark water by this day in December.

If not for the obvious bullish bias in all reportage everywhere (except alternative media), the market would have been declared a new bear market at that time (based on the market’s own historic standards where a 20% fall is a bear market), and any bull market after that would be a new bull market, not what is now called “the longest bull market on record.”

…click on the above link to read the rest of the article…

It’s Been a Great Recession for a Few; Let’s Do it All Again!

It’s Been a Great Recession for a Few; Let’s Do it All Again!

This month the economic expansion brought to you by your Federal Reserve and by US government largess becomes the longest expansion in the history of the United States! That’s something, right? Something? Let’s take an honest look at what we now call great.

By “the longest expansion” we mean the longest period in which US GDP has been growing without a recession. Now, that’s something to crow about, right?

Not so fast for many reasons. It’s also been the most anemic expansion on the books, and it’s not too hard to see why it’s been the longest, having nothing at all to do with a great economy. It has cost us far more than any expansion (by an order of magnitude) because we’ve piled up ten times the national debt over any amount we accumulated during previous expansions. (I’ve said before, it’s easy to let the “good times” roll when you are buying it all on the company credit card.) We also quadrupled the size of the size of the Fed’s balance sheet. That didn’t cost anything, but we sure didn’t get much bang for the buck! We actually got less bang than in any previous expansion!

The permanent recession

Sure, we got outstanding growth in stocks, but growth in business revenue has been pathetic. Growth in corporate development has been even worse (i.e., new plants, improved productivity, etc.) Growth in earnings was decent, except for the fact that it is entirely a feint because it was created mostly by reducing the numbers of outstanding shares over which earnings are divided, not so much by growing business. (Why do you think Wall Street prefers to talk about “earnings per share, ” EPS, instead of just actual profits?)

…click on the above link to read the rest of the article…

Liquidity Stress Fractures Begin to Show in the Federal Reserve System

Liquidity Stress Fractures Begin to Show in the Federal Reserve System

In my January Premium Post, “An Interesting Interest Conundrum,” I laid out how the Federal Reserve was losing control over the Fed funds rate — a loss of control over its bedrock interest rate that indicates financial stresses are building in the banking system that increase the risks from runs on the banks:

After the financial crisis, when there was a risk of runs on banks, the Fed … require[d] the banks to hold more money in reserves … as a regulation safeguard when the Fed was trying to avoid total economic collapse. Deposits, after all, are liabilities because depositors are guaranteed they can demand instant cash at will. Depositors get extremely unhappy if this guarantee is not fulfilled. That looks something like this:

And you don’t want that.

The Fed funds rate is the Fed’s target rate for the amount of interest banks charge each other to make overnight loans to each other from their reserves. In a crisis, when banks need their reserves, the interest they charge each other will naturally skyrocket. To keep the monetary system from freezing up because banks won’t loan to each other, the Fed tries to push that rate down.

During the Fed’s Great-Recovery bond-buying program (quantitative easing), aimed at pushing that rate down, the Fed deposited huge amounts of money created out of thin air into bank reserve accounts to make sure they remained flush so there would be no panic runs on banks, but banks don’t like just sitting on huge piles of money, instead of making even more loans with those piles, especially after the crisis abates. The Fed, however, wanted them to continue to maintain those reserves in case crisis returned.

…click on the above link to read the rest of the article…

A Week in the Life of a Topsy-Turvy Wildly Whirling World

A Week in the Life of a Topsy-Turvy Wildly Whirling World

![By Germán Torreblanca (Own work) [CC BY-SA 4.0 (https://creativecommons.org/licenses/by-sa/4.0)], via Wikimedia Commons](http://thegreatrecession.info/blog/wp-content/uploads/FatWomanSculpture1.jpg)

Let’s review this past devilishly whacky week to see if we can divine the way the world is turning and why the markets are churning. It was 2019’s worst week in stocks and, well, just about everything economic all across this crazily spinning planet. Volatility lifted its head back out of the water like Loch Ness’s monster while the citizenry took flight to treasury safe havens, bringing treasury yields down again to the five-year’s lowest point of the year. North Korea’s Rocketman returned to his rocketry, and the Chinese threw up their hands and ran as far from Mar-a-Lago as they could … or maybe they just threw up from too much chocolate cake.

The China syndrome is back

Most notably all over the world, bad news finally moved back to just being bad news, even as it arrived in cloudburst after cloudburst. Gold popped as money dropped and China flopped. Chinese exports fell 20%, outstripping the worst prediction four fold. The central bank of the billions of people of China mainlined major yuan jolts into the Xi dynasty’s tiring economy, and yet the Sino stock market fell off the mountain, taking a full panda bear plunge in one week. Apparently the nouveau riche Chinese ghost-city dwellers are wising up to all this easing and just realized talk of more of the same as far as the eye can see simply means the economy is finished more than it means refreshed hope waits on some distant horizon.

Trump talked and China walked. The best boast Trump could biggly bluster from his tweet blaster was that the stock market would rise again ifChina would only deal; China chose, instead, to cancel Chairman Xi’s second coming at Mar-a-Lago.

…click on the above link to read the rest of the article…

Epocalypse Ahead on Highway to Hell for Global Economy and US Stock Market

Epocalypse Ahead on Highway to Hell for Global Economy and US Stock Market

First I said I believed the US stock market would plunge in January, but I also said that January would not be the biggest drop, but just the first plunge that begins a global economic collapse: the big trouble for the economy and the stock market, I said, would show up in “early summer.” That’s when the stock market crash that began in January would take its second big leg down, and global economic cracks would become big enough that few could deny them.

(Now I’ll add a prediction — that even worse will unfold in the fall and early winter … unless summer becomes so bad that central banks rapidly reverse course on unwinding their balance sheets and raising interest; but I think they will stay their promised courses into the fall and winter and headlong into a global economic crisis.)

The stock market did plunge in January and on into February, with the Dow eventually taking its largest single-day point drop in its long history. That drop busted the Trump Rally, and the market never recovered, leaving US stocks (and stocks all over the world) shattered in “correction territory” for half a year. With a half a year for perspective now, here is a look back what that event did:

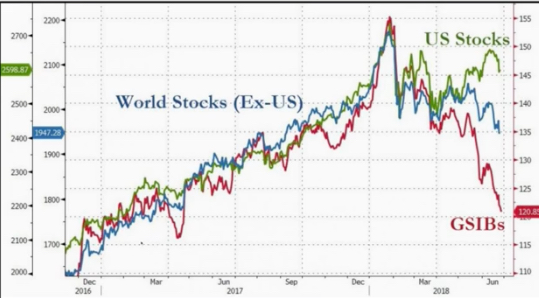

Global Stocks (except US), US stocks, and too-big-to-fail bank stocks. Where did the market trend abruptly change for all?

I’ve waited patiently through the first half of the year to talk in depth about how my January prediction faired because I felt we need many months in order to discern whether a trend has really been broken.

…click on the above link to read the rest of the article…

Return of the Euro Crisis: Italy Quakes, Rest of the World Shakes and Merkel’s Empire Breaks

Return of the Euro Crisis: Italy Quakes, Rest of the World Shakes and Merkel’s Empire Breaks

Europe’s many fault lines are spreading once again, bringing the endless euro crisis saga back in 3-D realism. Italy gained a new anti-establishment government last week, even as Spain elected a new Socialista government that could crack Catalonia off from the rest of Spain. All of Europe fell under Trumpian trade-war sanctions and threatened their own retaliation. And Germany’s most titanic bank got downgraded to the bottom of the junk-bond B-bin.

Europe’s many fault lines are spreading once again, bringing the endless euro crisis saga back in 3-D realism. Italy gained a new anti-establishment government last week, even as Spain elected a new Socialista government that could crack Catalonia off from the rest of Spain. All of Europe fell under Trumpian trade-war sanctions and threatened their own retaliation. And Germany’s most titanic bank got downgraded to the bottom of the junk-bond B-bin.

The Italian shakeup caused US bond prices to soar (yields to drop) in a flight of capital from European bonds, yet US stock investors took this invasion of troubles from foreign shores as good enough news to end the week on a positive note. The NASDAQ especially never looked happier, though financials feared contagion. As a result, the contrast between tech stocks and financials burst upward to its highest peak since the top of the dot-com frenzy:

While Europe’s troubles apparently sounded like great news to US stock investors, the Italian crisis caused EU bank stocks in aggregate to take one of their largest avalanches in history, ending in a one-week cliffhanger at their lowest level in two-and-a-half years. Deutsche Bank, Germany’s titan of global finance, ended looking like the spawn twin of the Lehman Brothers:

Deutsche Bank appears to be leading the way into a full blown euro crisis like Lehman Bros did in the US financial crisis.

In one week, Europe with its impossible euromess moved back into position of being the world’s chief menace. The Eurozone is a house of cards with many exits, each with their own name, as I’ve written about frequently in the past, and it’s time to pay the never-ending euro crisis some attention once again.

Quitaly looks like next Brexit in everlasting euro crisis

…click on the above link to read the rest of the article…

Federal Reserve Hesitates on QE Unwind / Balance Sheet Reduction

Federal Reserve Hesitates on QE Unwind / Balance Sheet Reduction

Is the Federal Reserve’s Great Unwind already coming unwound? I thought it would be good to check up on Federal Reserve balance sheet reduction since the Fed is supposed to be up and running on the move out of quantitative easing this month. It should be fascinating to see what progress the Fed is making as it happily applauds its own successful recovery.

Is the Federal Reserve’s Great Unwind already coming unwound? I thought it would be good to check up on Federal Reserve balance sheet reduction since the Fed is supposed to be up and running on the move out of quantitative easing this month. It should be fascinating to see what progress the Fed is making as it happily applauds its own successful recovery.

The Federal Reserve balance sheet reduction that didn’t happen

![By Kikuyu3 (Own work) [CC BY-SA 4.0 (http://creativecommons.org/licenses/by-sa/4.0)], via Wikimedia Commons](http://thegreatrecession.info/blog/wp-content/uploads/Hommage_to_the_Gordian_knot-300x225.jpg)

Is balance sheet reduction the Fed’s Gordian knot?

After all, the Federal Reserve’s End of Quantitative Easing Didn’t Happen last time they said it would. It turned out the Fed actually planned to continue QE at a gradual level by reinvesting matured assets. Nevertheless, the mere announcement in 2013 that it would terminate QE in 2014 created the infamous “Taper Tantrum.” The Fed hadn’t said anything back then that I was able to find about reinvesting the funds in its balance sheet until after they supposedly stopped QE in the fall of 2014. It turned out the stop was not a quite a full stop.Unwinding its balance sheet is likely to prove to be the Fed’s Gordian knot.

Federal Reserve balance sheet reduction that didn’t happen … again … so far

So, here we are, and so far there is no reduction. It is now three years since the Fed “ended quantitative easing,” and its balance sheet is still holding around the $4.5 trillion mark where QE was supposed to end. Now that’s gradual! It’s taken three years just for the Fed to say it is going to start reducing the balance; so, let’s see how that balance sheet reduction is going for them now that it has supposedly started:

…click on the above link to read the rest of the article…

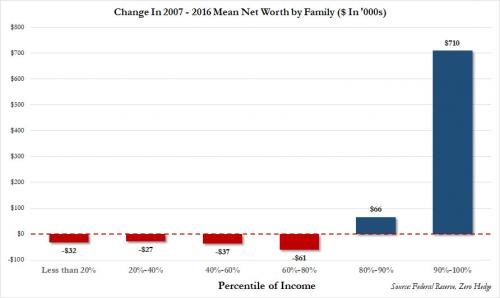

Here’s You and Here’s the Top Ten Percent

Here’s You and Here’s the Top Ten Percent

In a nutshell, here is a graph that summarizes everything you need to know about the unsustainable US economy. Unless you’re in the top ten percent of income producers in the nation — or, at least, living in their neighborhood — you are living in a dingy bedroom economy that has only seen its net worth decline since the Great Recession began. Those who are in the top ten percent, on the other hand, profited astronomically from the Great Recession. It’s the best thing that ever happened to them, and you helped them do it with tax-backed or even tax-funded bailouts and by allowing them a perpetual cycle of savings on their capital gains.

In a nutshell, here is a graph that summarizes everything you need to know about the unsustainable US economy. Unless you’re in the top ten percent of income producers in the nation — or, at least, living in their neighborhood — you are living in a dingy bedroom economy that has only seen its net worth decline since the Great Recession began. Those who are in the top ten percent, on the other hand, profited astronomically from the Great Recession. It’s the best thing that ever happened to them, and you helped them do it with tax-backed or even tax-funded bailouts and by allowing them a perpetual cycle of savings on their capital gains.

Clearly the only ones who “recovered” are at the top

Insanity is repeating the same thing over and over and expecting different results

Now you can see how those bailouts have trickled down to you as well as how capital-gains tax breaks have trickled down. Are you now going to go for Trump’s third-and-greatest-ever round of trickle-down economics?

Lower taxes for corporations may be a good idea (why tax the economic engines and rob them of fuel) if they also come with the end of loopholes (corporate welfare) and with a provision that the corporation cannot be engaged in any corporate buybacks during that tax year or the following. (Without that provision, lower corporate taxes will just fuel useless stock buybacks, making the rich richer, but doing nothing to grow the corporation and grow jobs).

Capital-gains tax breaks, on the other hand, have always been a terrible idea. The notion that such breaks cause people to reinvest their tax savings into creating new factories and jobs is not only proven wrong by thirty-plus years of history (see chart above for just the last decade of decline), but it is ludicrous in concept (even without historic proof):

…click on the above link to read the rest of the article…